Discover essential insights on Spain digital nomad visa taxes. Avoid costly mistakes and learn how tax residency affects your income.

Spain’s Digital Nomad Visa taxation is governed primarily by whether you qualify for the Beckham Law, a special regime offering a flat 24% tax rate on Spanish-source employment income up to €600,000. Without it, you fall under Spain’s standard progressive personal income tax (IRPF) system, where rates climb as high as 47%. Understanding spain digital nomad visa taxes before you arrive is not optional. The difference between these two regimes can mean tens of thousands of euros per year, and the window to elect the better option closes fast.

What are the Spain digital nomad visa taxes you actually owe?

Spain’s tax system does not automatically assign you a rate when you arrive. Your obligations depend on two separate determinations: whether you become a Spanish tax resident, and which tax regime applies to you.

The Digital Nomad Visa does not confer tax residency by itself. Spanish tax residency kicks in when you spend more than 183 days in Spain in a calendar year, when your primary economic interests are based there, or when your family lives there. You can hold the visa and still be a non-resident for tax purposes if you spend most of the year elsewhere. That distinction matters enormously for what you file and how much you pay.

Once you cross the residency threshold, you must file Spanish income taxes. The regime that applies, Beckham Law or standard IRPF, determines your effective rate. Many digital nomads mistakenly assume the visa alone dictates their tax treatment. It does not. Income source definitions and residency rules govern your actual liability.

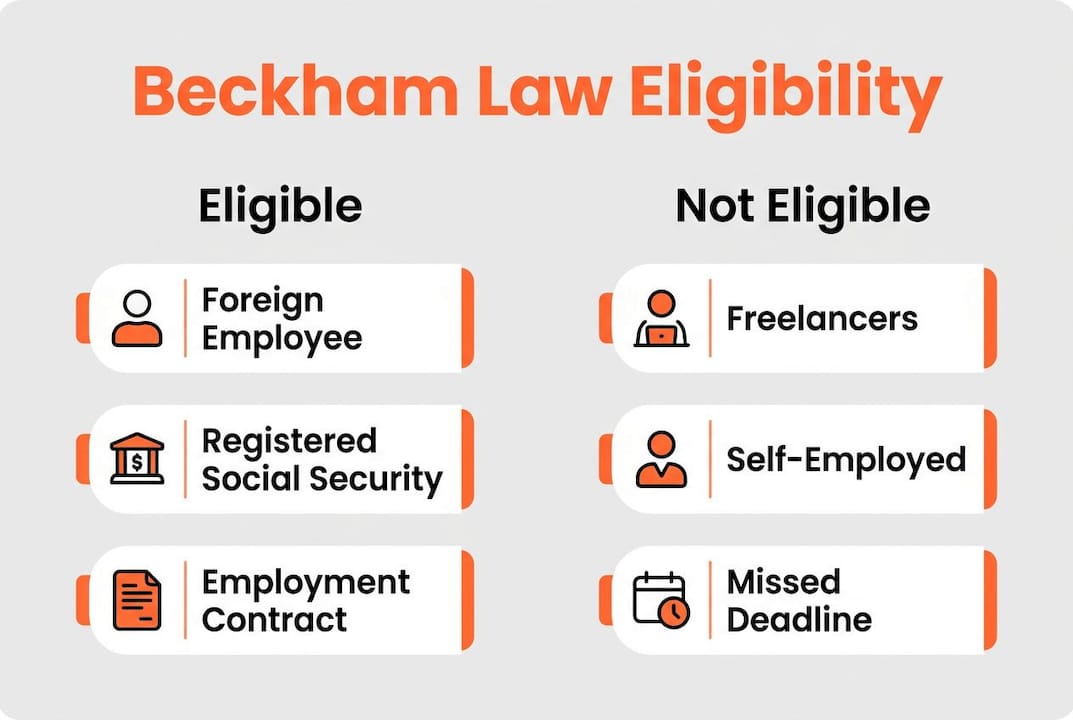

Who qualifies for the Beckham Law under the Digital Nomad Visa?

The Beckham Law, formally known as the Special Expatriate Tax Regime, is the most tax-efficient pathway available to Digital Nomad Visa holders who meet its conditions. The combination of the Digital Nomad Visa with the Beckham Law is one of the most advantageous setups for international remote workers in Europe right now.

Core eligibility requirements

To qualify, you must meet all of the following:

- You must not have been a Spanish tax resident in the previous five years before your arrival.

- You must work as an employee for a foreign company or a Spanish company with international operations. Freelancers and self-employed workers are excluded.

- No more than 20% of your total income can come from Spanish sources.

- You must file Form 149 (Modelo 149) within six months of registering with Spanish Social Security.

The employment requirement is the most common disqualifier. If you work as a freelancer billing clients directly, you do not qualify for the Beckham Law regardless of your visa status.

What happens if you miss the deadline?

Form 149 is a binding, non-extendable declaration that activates the Beckham Law retroactively from the first day of your tax residency year. Miss the six-month window and you permanently lose access to this regime for your current residency period. There is no appeal, no extension, and no workaround. That single administrative deadline is the most consequential date in your entire Spanish tax calendar.

Pro Tip: Register with Spanish Social Security as soon as possible after arrival and immediately calendar your Form 149 deadline. Do not wait until month five.

Tax rates and filing requirements for Digital Nomad Visa holders

The difference in rates between the two regimes is stark and worth spelling out clearly.

Beckham Law rates and forms

Under the Beckham Law, Spanish-source employment income up to €600,000 is taxed at a flat 24%. Income above that threshold is taxed at 47%. Foreign-source employment income is generally exempt from Spanish tax for the duration of the regime. The Beckham Law election applies for six tax years: the year of arrival plus the following five years. After that, standard IRPF rules resume.

The key forms under this regime are:

- Modelo 149: The opt-in declaration. Filed within six months of Social Security registration.

- Modelo 151: The annual tax return for Beckham Law taxpayers. Filed between april and june each year.

Standard IRPF rates and forms

Without the Beckham Law, you file under Spain’s progressive IRPF system. Rates run from 19% on the first €12,450 of income up to 47% on income above €300,000. Foreign-source income is also taxable under this regime, which significantly raises the effective burden for nomads earning abroad.

The standard annual return is Modelo 100, filed in the same april to june window as Modelo 151.

| Tax regime | Rate on Spanish income | Foreign income | Annual form |

|---|---|---|---|

| Beckham Law | 24% flat (up to €600,000) | Generally exempt | Modelo 151 |

| Standard IRPF | 19%–47% progressive | Fully taxable | Modelo 100 |

One additional obligation applies regardless of regime. Spanish tax authorities require filing Modelo 720 if your foreign assets exceed €50,000. This catches many nomads with offshore investment accounts or foreign property off guard.

Pro Tip: If you hold foreign brokerage accounts, pension funds, or real estate abroad, calculate your total asset value before your first Spanish tax year ends. Filing Modelo 720 late carries steep penalties.

What taxes do self-employed digital nomads pay in Spain?

Self-employed digital nomads, registered as autónomos in Spain, face a significantly heavier tax burden than their employee counterparts. The Beckham Law does not apply to freelancers or self-employed workers. Every euro of worldwide income is subject to standard progressive IRPF rates from 19% to 47%.

The Social Security obligation compounds this. Self-employed nomads pay Social Security contributions based on real income, typically between €500 and €800 per month. That translates to roughly €6,000 to €9,600 per year in contributions alone, before a single euro of income tax is calculated.

The dual tax challenge for autónomos

Autónomos face dual tax challenges: high progressive IRPF rates on worldwide income alongside mandatory monthly Social Security contributions. The combined effective burden is substantially heavier than what an employee on the Beckham Law pays.

Key obligations for self-employed Digital Nomad Visa holders include:

- Quarterly IRPF advance payments (Modelo 130) due in april, july, october, and january.

- Quarterly VAT returns (Modelo 303) if providing services to Spanish clients.

- Annual income declaration via Modelo 100.

- Monthly or quarterly Social Security contributions based on declared net income.

One partial relief option is a totalization agreement. Spain has bilateral Social Security agreements with several countries, including the United States. If you are already contributing to Social Security in your home country under a totalization agreement, you may avoid double contributions. This requires documentation and advance coordination, not a retroactive fix.

How do you avoid costly mistakes with Digital Nomad Visa taxation?

The most expensive tax mistakes nomads make in Spain are not about rates. They are about timing and structure.

The six-month deadline is absolute

The Beckham Law election requires filing Form 149 within six months of Spanish Social Security registration. No extensions exist. Missing this deadline means paying standard IRPF rates for your entire residency period under that visa. For a nomad earning €80,000 per year, the difference between 24% flat and a progressive rate averaging 35% to 40% is not trivial.

Timing your arrival strategically

Your tax residency year begins on the date you establish residency, not the date you arrive in Spain. Arriving in october rather than january means your first Spanish tax year covers only three months. That gives you more time to plan your income streams and structure before a full tax year begins. This is a legitimate and widely used planning approach.

US citizens face an additional layer

US citizens with a Spain Digital Nomad Visa may owe US tax on worldwide income even while paying Spanish taxes. The Foreign Earned Income Exclusion can offset a portion of US liability, but the interaction with the Beckham Law is complex. Income exempt under Beckham Law in Spain may not qualify for the Foreign Tax Credit in the US, creating a gap that requires expert coordination.

- Confirm your Social Security registration date immediately upon arrival.

- File Form 149 within six months of that date, not six months from your visa approval.

- Analyze your income sources before arrival to confirm the 20% Spanish-source income limit.

- Engage a Spanish tax advisor with Digital Nomad Visa experience before your first tax year ends.

- Check totalization agreements if you are self-employed and already contributing abroad.

- Declare foreign assets above €50,000 via Modelo 720 before the deadline.

Pro Tip: Professional tax and legal coordination is vital because the Beckham Law election is not automatic. Structural income and residency planning before arrival can save more than any post-arrival optimization.

Key Takeaways

Spain’s Digital Nomad Visa tax outcome depends almost entirely on Beckham Law eligibility, the six-month Form 149 deadline, and whether you work as an employee or self-employed.

| Point | Details |

|---|---|

| Beckham Law flat rate | Employees pay 24% on Spanish-source income up to €600,000; foreign income is generally exempt. |

| Six-month Form 149 deadline | Missing this window permanently eliminates Beckham Law access for your current residency period. |

| Self-employed exclusion | Autónomos pay progressive IRPF up to 47% plus €500–€800/month in Social Security contributions. |

| Visa vs. tax residency | The Digital Nomad Visa does not create tax residency; 183 days in Spain triggers that obligation. |

| Modelo 720 requirement | Foreign assets above €50,000 must be declared regardless of which tax regime applies. |

Why the Beckham Law deadline is the one thing I tell every nomad first

When nomads ask me what they need to know about Spain’s tax system, I skip the rate tables and go straight to one date: the Form 149 deadline. Every other tax question has a workaround or a correction mechanism. That deadline does not.

I have seen nomads arrive in Spain with solid employment contracts, legitimate Beckham Law eligibility, and every intention of filing correctly. Then life gets busy. They delay registering with Social Security. They assume the visa process and the tax process are the same thing. Six months pass. The window closes. They spend the next six years paying standard IRPF on income that could have been taxed at 24%.

The other thing I push hard on is the visa-versus-residency distinction. Your Digital Nomad Visa requirements and your tax residency status are governed by completely separate legal frameworks. Conflating them is the single most common and costly conceptual error I see. You can hold the visa and not be a tax resident. You can be a tax resident before your visa is even approved. These are not the same clock.

Spain’s tax rules for nomads are genuinely favorable if you qualify for the Beckham Law and act on time. The regime is not a loophole. It is a deliberate policy to attract international talent. Use it correctly, and Spain becomes one of the most tax-efficient places in Europe to base yourself. Ignore the deadlines, and it becomes one of the most expensive.

— Joshua

How Digitalnomadinspain helps you get the tax setup right

Navigating Spain’s Digital Nomad Visa tax obligations requires more than reading a guide. The Beckham Law opt-in window, Social Security registration timing, and income source analysis all need to happen in a specific sequence before your first Spanish tax year ends.

Digitalnomadinspain provides end-to-end support for Digital Nomad Visa applicants, including eligibility screening, document preparation, and guidance on Beckham Law filing requirements. With a 98% success rate and processing times typically 30% faster than self-applicants, the team has helped remote workers from over 50 countries establish compliant, tax-efficient residency in Spain. Check your eligibility and get your application started at Digitalnomadinspain.

FAQ

What is the Beckham Law tax rate for Digital Nomad Visa holders?

The Beckham Law applies a flat 24% rate on Spanish-source employment income up to €600,000 per year. Income above that threshold is taxed at 47%, and foreign-source employment income is generally exempt.

How long does the Beckham Law last?

The Beckham Law regime covers six tax years total: the year you establish Spanish tax residency plus the following five years. After that, standard progressive IRPF rates apply.

Can freelancers use the Beckham Law with a Digital Nomad Visa?

No. The Beckham Law excludes self-employed workers and freelancers. Only employees working for a foreign company or a qualifying Spanish employer can elect this regime.

What happens if I miss the Form 149 deadline?

Missing the six-month Form 149 filing window permanently disqualifies you from the Beckham Law for your current residency period. No extensions or retroactive applications are permitted.

Does the Digital Nomad Visa automatically make me a Spanish tax resident?

No. The Digital Nomad Visa does not confer tax residency. Spanish tax residency is triggered by spending more than 183 days in Spain, having your primary economic interests there, or having your family based there.